- Alternative Data

- Market Data Approach

The SMACOM Risk-Related "Accrual Score" Predicts Accounting Fraud

It is no exaggeration to say that everyone who conducts stock asset management checks financial statements and certain other essential financial data sources when selecting investments. In particular, special attention is generally given to fundamental indicators such as profit margins. Even if these are not accorded preeminent status by some asset managers, it is clear that they provide indispensable information for evaluating growth potential and risk.

However, how can we be assured of the veracity of the financial data underpinning core calculations? While it may be possible to confirm that accurate financial statements have been disclosed, such as through audit certificates, there are a small number of companies that slip past third-party confirmation, commit accounting fraud, and deceptively make their financial statements look better than they should. Some companies have been the targets of recommendations from the Securities and Exchange Surveillance Commission (SESC) for surcharge payment orders, and in serious cases, businesses have even been prosecuted. To avoid such outcomes, a model that evaluates accounting fraud risk with a high degree of certainty can be used.

SMACOM, provided by Nikkei Financial Technology Research Institute (or Nikkei FTRI), has three scores that can be used to evaluate risk. In this article, we examine the screening of investment targets using the Nikkei FTRI's "Accrual Score" risk evaluation model.

The Accrual Score quantifies accounting fraud risk, indicating the probability that a subject company is involved in accounting fraud or earnings management. Scores vary from 1 to 100, with the higher the score, the lower the probability that the company is committing accounting fraud. Previously, Nikkei FTRI delivered a product called the "Accounting X-Ray" to many financial institutions and auditing firms for accounting fraud screening in Japan. The company developed the Accrual Score based on the knowhow it accumulated in this area.

The AR value is an indicator for evaluating the ability of a model to determine corporate events. It is expressed as a number between 0 and 1, where the closer the value is to 1, the more capable the model in question is deemed to be at detecting companies that may have been charged or recommended for surcharge payment order by the SESC. Usually, a model with an AR value of 0.6 or higher can be used to assist those making default judgments. The AR value of the Accrual Score is 0.6896, which means it is considered to be an excellent tool for identifying potential accounting fraud.

Even when a given company's stock price is firm, it is still possible that it has adjusted its profits and/or engaged in accounting fraud. This is one scenario that highlights the difficulty of selecting stocks for investment. Stock prices may not factor in the risk of accounting fraud, and suddenly it can be revealed that a company has engaged in window dressing. From this point, the company goes bankrupt, its stock price plummets, and the opportunity to sell is not secured. To avoid this gloomy outcome, it is advisable to make effective use of the Accrual Score.

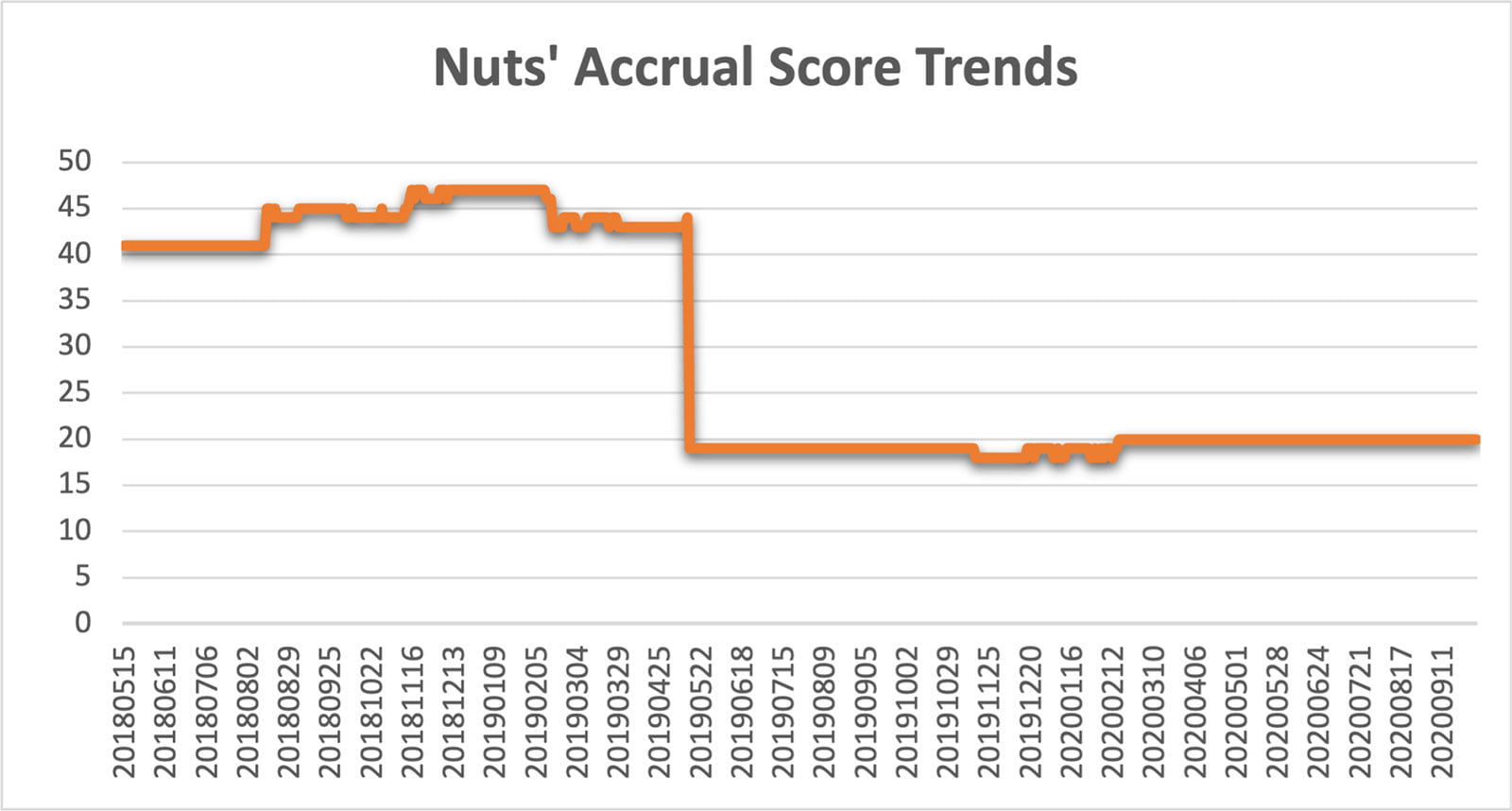

Now, considering the question of whether accounting fraud can actually be predicted, let's look at changes in the Accrual Score for Nuts Inc. (3606). Accounting fraud was uncovered at this company in 2020, and it subsequently went out of business.

Nuts was established in 1977 to sell vinyl chloride products, following which it entered the rental business for video software and other products in 1982. Nuts began game software sales in 1989, and later it delved into pachinko and pachislot business activities, acquiring exclusive licensing rights to convert devices used for these pursuits into medal game machines and to sell them. In 2016, the company changed its name to Nuts Inc. However, its business subsequently stagnated, and in 2017, the company entered the healthcare-related field and specialized in consulting focused on the management of healthcare facilities. However, results did not improve, and the company posted losses for four consecutive fiscal years starting in 2016. In February 2020, the company was the subject of mandatory investigation and suspected of violating the Financial Instruments and Exchange Law. The announcement of financial results for the fiscal year ending March 2020 was postponed and padding of cash was also discovered in the audit process. Then, on September 16, 2020, the directors of Nuts filed for bankruptcy with the Tokyo District Court, and on the same day the decision to commence bankruptcy proceedings was made.

The Accrual Score for Nuts sharply decreased from 44 to 19 points in mid-May 2019. Before this, the score had been in the 40-point range, which could be interpreted as a sign that accounting fraud was possible but not highly likely. However, the decrease to 19 points can be understood as a stronger indication that Nuts had been conducting accounting fraud; according to a report by the external investigation committee published in September 2020, fictitious transactions identified by said committee began in April 2019. We can see that the Accrual Score reacted accordingly, meaning that this metric indeed reflected the possibility of accounting irregularities at Nuts. This confirms that SMACOM's Accrual Score is a valid predictor of potential accounting fraud.

By utilizing the Accrual Score for stock selection, not only will you be able to pursue higher performances - you can also to increase the likelihood of more stable investment results.

Nikkei FTRI is currently offering a free trial of SMACOM. If you are interested, please contact us by clicking below:

https://www.ftri.co.jp/eng/index.html#company

Disclaimer (PDF file):

https://www.ftri.co.jp/eng/pdf/SMACOM_Disclaimer-EN.pdf

Nikkei FTRI

Nikkei FTRI is a member of the Nikkei Group that works with data analysis technology. We are recognized for the high quality of our analytical and modeling techniques, which utilize both traditional and alternative varieties of data.

See More