- TOP

- Stories

- The Combination of News Sentiment and Access Ranking Scores, and Resulting Applications to Equity Investment

- Alternative Data

- Market Data Approach

The Combination of News Sentiment and Access Ranking Scores, and Resulting Applications to Equity Investment

With the rapid development of machine learning in recent years, NLP (Natural Language Processing) has been ever further applied to the financial field*1 . We posted a certain article ("SMACOM's unique 'News Sentiment Score'") in January 2022*2. It related to our examination of whether news sentiment scores that had been calculated through NLP and neural network technology had cross-sectional predictive power in relation to stock returns. Such scores evaluated whether the news released by NIKKEI and/or QUICK was positive, negative, or neutral about a given firm's predicted future performance. In this paper, we will demonstrate how we extracted necessary information from news sentiment scores strongly related to stock prices.

To begin with, the following points were made about the news. First, it was noted that the news does not necessarily address readers' (i.e., investors') interests as it depends on journalists (i.e., producers of news). Second, we recognized the difficulty of news to cover all the interests of readers/investors. If a proxy variable for investors' interests were to be combined with a news sentiment score, it would be possible to extract information that could strongly impact stock prices. Therefore, Quick access ranking data were chosen as a proxy for investors' interests. Data was based on access frequency in relation to specific stocks on the Quick platform. The top 100 access rankings and their security codes as well as their proportional shares of all accesses were provided. For this paper, we created a composite score combining access ranking with news sentiment score and checked its validity in terms of cross-sectional return forecasting.

To create the composite score, first we examined the characteristics of the news sentiment score and the access ranking score. The news sentiment score ranges from -50 to +50, with a higher (lower) value indicating that the news is more positive (negative) in relation to the company's predicted future performance. For the access ranking score, we used the top 100 companies ranked by access frequency. Both the news sentiment score and the access ranking score were calculated on a daily basis.

*1 Examples of applications of alternative data to the finance field

Amen, S. (2018). Robo-news reader - Using machine-readable Bloomberg News to trade FX

Amen, S. (2016). Trading Anxiety. Retrieved from Investopedia

*2 https://www.nikkei.co.jp/nikkeiinfo/en/global_services/nikkei-ftri/smacoms-unique-news-sentiment-score.html

Next, let us consider how to synthesize these scores. For this paper, we simply used the access ranking (top100) for filtering those stocks assigned news sentiment scores. It can be interpreted that a high news sentiment score within the top 100 access ranking signifies positive news accompanied by investor interest.

The backtesting using the composite score was performed as described below. The investment universe was composed of all the stocks listed in Japan (including REITs), and the backtest sample period was from September 30th 2020 to January 31st 2023. The rebalancing frequency was daily, and transaction costs were not considered. When using only news sentiment score, we went long on stocks with scores in the top 10% and short on those scoring in the bottom 10%. For the composite score, we were long on stocks with positive scores and short on those scoring in the bottom 25%. Since the news sentiment score is released around 12:30 p.m. on a daily basis (with the access ranking score being released every 30 minutes), we assumed that we were trading at 3:00 p.m. closing prices using data from 12:30 p.m. on the same day for both the news sentiment score and the access ranking score.

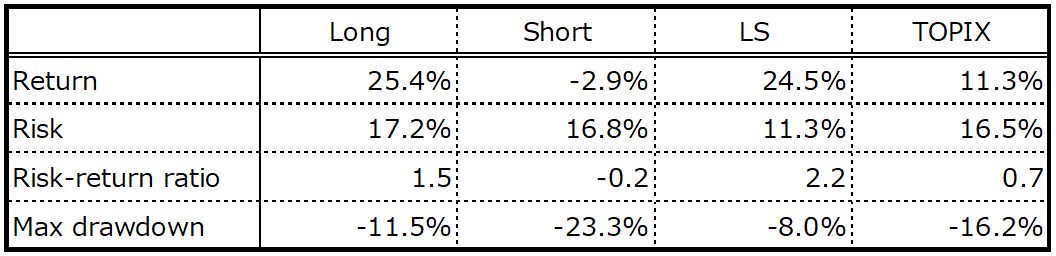

Table 1 Performance with news sentiment score only

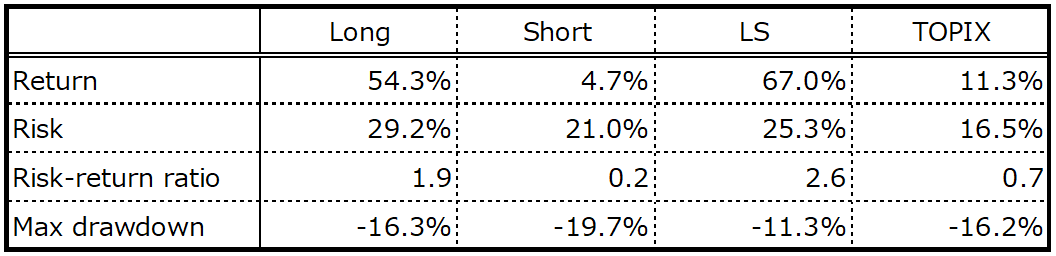

Table 2 Performance with composite score (news sentiment + access ranking)

Table 1 and table 2 show the performance in the long ("Long" in the table), short ("Short" in the table), and long-short ("LS" in the table) categories using only news sentiment score and composite score, respectively. The performance of TOPIX ("TOPIX" in the table) is also provided for comparison.

The results demonstrated that the news sentiment score (Table 1) performed favorably. The score worked well on the long side with a return of +25.4%. On the short side, the return was slightly negative (-2.9%), with the TOPIX return in the same period being +11.3%. LS (long-short) posted a higher risk-return ratio (close to 2.2) than Long alone due to a benefit of diversification with a maximum drawdown of just -8.0%.

Next, turning to the composite score (Table 2), the return on the long side more than doubled to 54.3% in comparison with the figures in with Table 1. Likewise, the performance on the short side improved to 4.7% from -2.9%. Therefore, it was indicated that the access ranking score strengthened the information associated with the news sentiment score, especially on the long side, during the backtest period. LS (long-short) posted a higher return of 67.0%, but its related risk was also higher than was the case with news sentiment alone. Nevertheless, this yielded a better risk-return ratio of 2.6. The increase in risk was due to the fact that the top 100 access ranking restricted the number of stocks in both the long and short categories, leading to higher idiosyncratic risks.

In this paper, we have described how we confirmed that the news sentiment score exhibited strong cross-sectional return predictive power, especially on the long side. Also confirmed was the fact that the access ranking score reinforced the information associated with the news sentiment on the long side. Although we used the access ranking score as a proxy for investors' interests, other factors could help strengthen the cross-sectional predictive power of the news sentiment score in relation to stock returns. We will undertake further work to introduce such factors and discern their relationships with the news sentiment score.

SMACOM: https://www.ftri.co.jp/product/smacom/en

SMACOM free trial (below):

https://www.ftri.co.jp/eng/index.html#company

Disclaimer (PDF file):

https://www.ftri.co.jp/eng/pdf/SMACOM_Disclaimer-EN.pdf

Nikkei FTRI

Nikkei FTRI is a member of the Nikkei Group that works with data analysis technology. We are recognized for the high quality of our analytical and modeling techniques, which utilize both traditional and alternative varieties of data.

See More