- Alternative Data

- Market Data Approach

SMACOM's new quality score under development

As discussed in an earlier article, factor investing has been researched and subjected to experimentation, especially in equity markets, and it has been widely deployed in the asset management world. While our previous focus in this area was on momentum factor, here we will discuss quality factor, which is another major topic in the world of factor investing.

Although there is no firm definition of the quality factor, it can be seen as a measure of a company's ability to increase future value for shareholders. It can be broken down into two categories - one is competitiveness in terms of business economics, and the other is the competency of company management. Business economics competitiveness normally stems from efficient operations, intellectual innovation and/or market dominance, all of which enable the generation of profits in excess of the cost of capital. The competency of company management relates to matters arising from agency issues and is an indication of how effectively managers act to increase shareholder value as opposed to operating based on personal interest.

To take some examples, profitability can serve as a proxy for a company's competitiveness. A higher value indicates a higher return on invested capital compared with peer group members. Management competency (i.e., relating to agency problems) is often measured by proxies such as profit manipulation, overinvestment and excessive external financing. The presence or absence of such factors indicates whether the management is acting on its own behalf at the expense of the shareholders.

As with previously noted issues related to momentum factor, this paper regards market beta, size and book-to-market ratio plus size-related nonlinear factors as systematic risk factors, following Fama and French (1993). It examines whether quality factor information excluding such risk factors has cross-sectional predictive power in relation to stock returns.

Three quality factors - profitability-based, agency-problem-based and payout-based (dividends and buybacks) - are chosen as alphas. These are risk-adjusted alphas constructed using our own methodology to exclude the four systematic risk factors noted above. The investment ratio (or weight) of each stock has been calculated with the assumption that the target portfolio risk is 5% annually. The investment universe is composed of the stocks listed on the Tokyo Prime market (i.e., what was formerly known as the first section of the TSE), excluding those in the financial sector, and the backtesting sample period is from January 2007 to October 2022. The rebalancing frequency is monthly, and transaction costs are not considered.

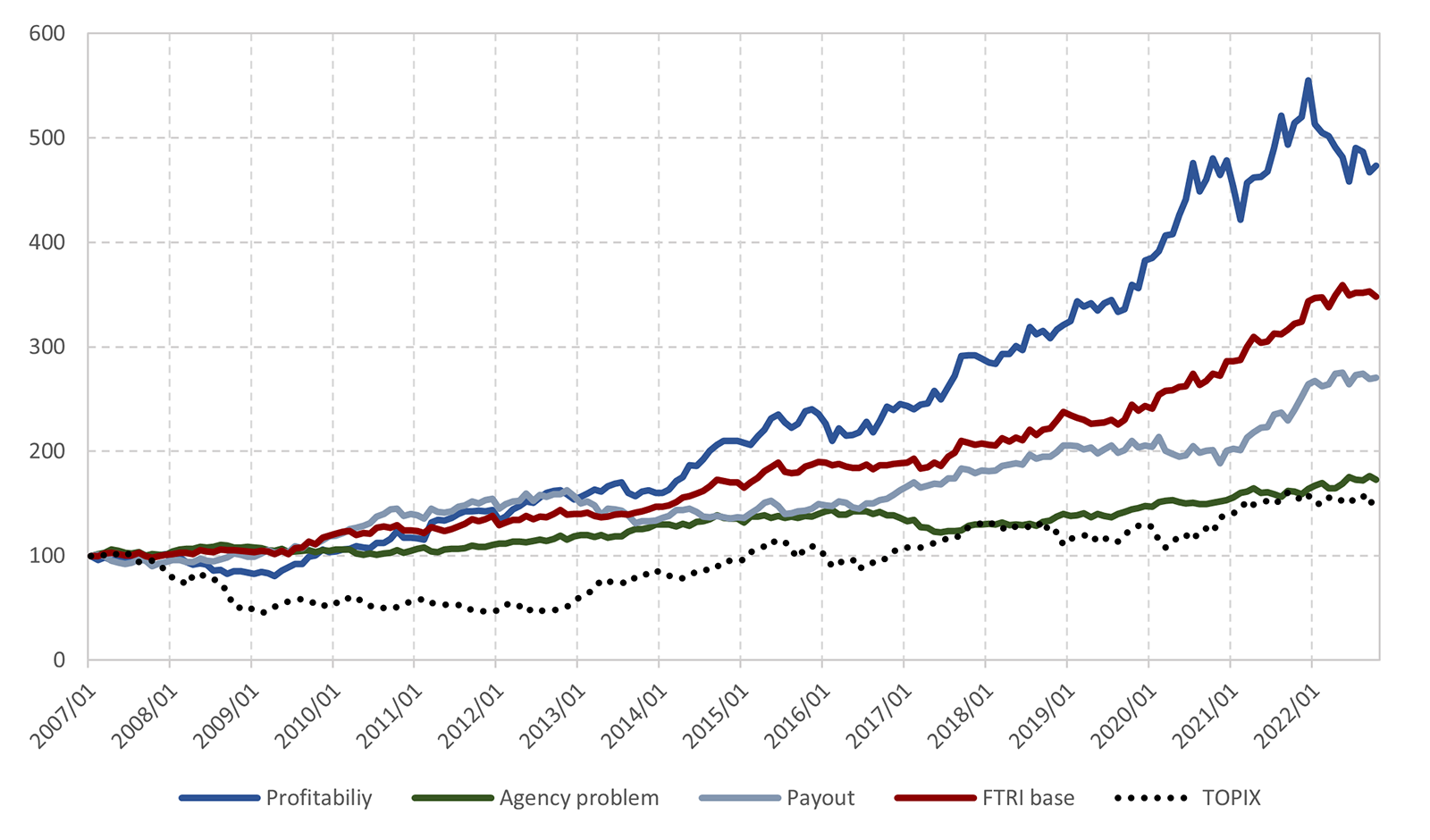

Figure 1 Performance of quality factors

Source: FactSet

Figure 1 shows the performance of each quality factor, plus an FTRI-based factor that is a composite thereof. The composite weight is calculated according to original FTRI methodology. "TOPIX" indicates TOPIX, including dividends, as a reference. The results demonstrate that all of the factors outperformed TOPIX. Profitability factor shows the best performance at about 10.38% annualized return, and its risk-return ratio (or information ratio) is 0.86. Agency problem factor, on the other hand, indicates the lowest return at 3.53%, and its risk is also the lowest. As a result, its risk-return ratio is 0.61 and is much higher than that of TOPIX's 0.16. With respect to payout factor, the performance is somewhere between profitability factor and agency problem factor.

Next, note that the risk-return ratio for the FTRI-based factor is 1.08, which demonstrates a higher risk-adjusted return. This suggests that the correlation among the quality factors, especially between agency problem factor and the others, is low (i.e., negative), which may be the causal element accounting for a more efficient portfolio with lower risk.

The value and momentum factors were the focus of the two previous articles, and the quality factor has been discussed here. The final matter of discussion is the supposition that a composite thereof (i.e., the value, quality and momentum factors) based on the IC (Information Coefficient) can lead to a more efficient portfolio from a risk-return perspective.

SMACOM: https://www.ftri.co.jp/product/smacom/en

SMACOM free trial (below):

https://www.ftri.co.jp/eng/index.html#company

Disclaimer (PDF file):

https://www.ftri.co.jp/eng/pdf/SMACOM_Disclaimer-EN.pdf

Nikkei FTRI

Nikkei FTRI is a member of the Nikkei Group that works with data analysis technology. We are recognized for the high quality of our analytical and modeling techniques, which utilize both traditional and alternative varieties of data.

See More