- Alternative Data

- Market Data Approach

SMACOM Risk-Related "Credit Score" Predicts Management Failure

To achieve outstanding performance in asset management focused on stocks, it is necessary to take commensurate risks. Thus, high-risk, high-return investment is often the basic principle at work in this endeavor. There are two types of risk that such investors take - the risk that stock prices will fall, and credit risk, which is associated with the possible failure of a company that is an investment target. The former risk involves an element of uncertainty because it is affected by the actions of an unspecified number of investors. However, credit risk can be ameliorated to a significant extent by using a valuation model that demonstrates a high degree of reliability.

SMACOM, provided by Nikkei Financial Technology Research Institute (or Nikkei FTRI), has three scores that can be used to evaluate risk. In this article, we examine the screening of investment targets using the Nikkei FTRI's "Credit Score" risk evaluation model.

The Credit Score is a numerical value used to quantify a company's credit risk, indicating the probability of default in one year. Scores vary from 1 to 100, with the higher the score, the lower the probability of default. Nikkei FTRI originally developed this form of measurement based on its expertise with risk models used for credit management by banks.

The default discrimination ability of a credit risk model is evaluated using a figure between 0 and 1 known as the AR value, which allows judgement of the effectiveness of a model in determining default. Customarily, models with AR values of 0.6 or higher are used, but if the number exceeds 0.9 for a given model, it is sensitive only to defaults occurring under the same conditions used to create it, making it difficult for the model to predict defaults that have never been experienced. The AR value of SMACOM's Credit Score is 0.8281, which is considered to represent an ideal default discrimination ability.

In some cases, credit risk increases in the near term, even when stock prices are firm. In this situation, the difficulty of selecting stocks for investment comes to the surface. When the stock price does not factor in the credit risk, and if the company suddenly goes bankrupt, the stock price plummets without giving investors the opportunity to sell the shares held. To avoid such a situation, it is advisable to make effective use of the Credit Score.

To determine whether default can actually be predicted in this way, an instructive case is provided by the Credit Score activity of Renown Inc. (3606), a Japanese manufacturer that went out of business in 2020.

Founded in 1902, Renown was a longstanding apparel company in Japan; indeed, in the 1990s, it was one of the world's largest such companies. However, its business model was based mainly on department store sales, and this strategy had become increasingly untenable over the years with the rise of Internet shopping and fast fashion. After two consecutive fiscal years of losses, Renown entered a state of default. Due to the spread of the coronavirus, department stores with tenant shops were forced to suspend operations, resulting in a sharp decline in apparel sales. Faced with a dearth of cash, the company filed for bankruptcy on May 15, 2020.

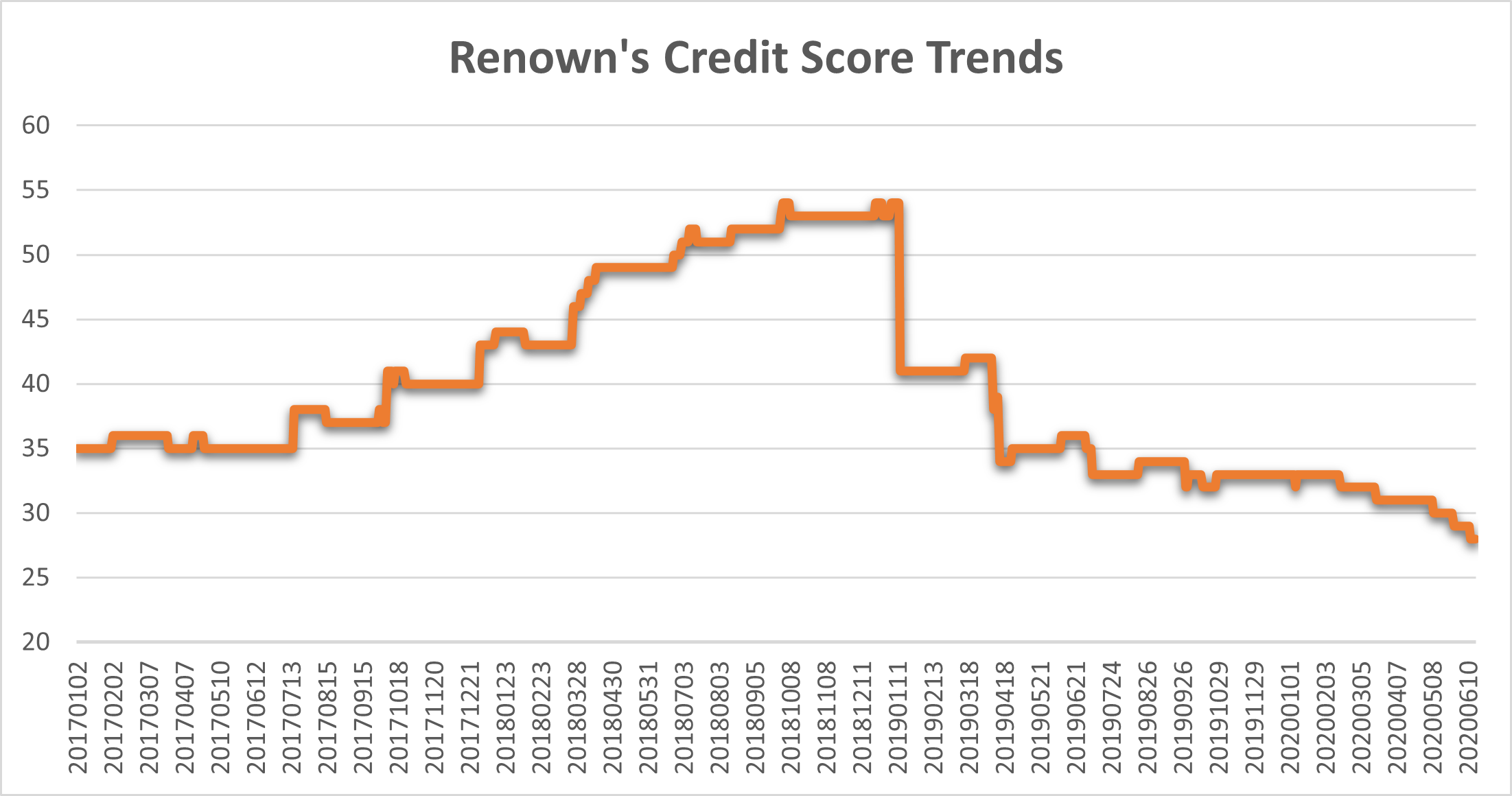

The trends in the Credit Score accurately indicated the rise of Renown's default risk, as can be seen in the above chart.

Around October 2017, when performance improved, Renown's Credit Score increased as the likelihood of default correspondingly decreased. The situation suddenly changed in January 2019, when the Credit Score plummeted from the 50s to the 40s. After this, there were no further signs of improvement, and the score had dropped to the low 30s by April 2019. Renown subsequently initiated a voluntary retirement program among its employees in August 2019, and in February 2020, the company issued a going concern note. The sharp decline in the company's Credit Score six months earlier had sounded the alarm about the possibility of future defaults. Renown's failure occurred in May 2020, almost one year after its Credit Score had fallen to the 30s.

As noted, SMACOM's Credit Score can serve as a valid predictor of default of a company one year in advance, and Renown's example is a perfect example of this. Use of the Credit Score in selecting stocks clearly enables the pursuit of stronger and more stable investment performance.

Nikkei FTRI is currently offering a free trial of SMACOM. If you are interested, please contact us by clicking below:

https://www.ftri.co.jp/eng/index.html#company

Disclaimer (PDF file):

https://www.ftri.co.jp/eng/pdf/SMACOM_Disclaimer-EN.pdf

Nikkei FTRI

Nikkei FTRI is a member of the Nikkei Group that works with data analysis technology. We are recognized for the high quality of our analytical and modeling techniques, which utilize both traditional and alternative varieties of data.

See More