- Alternative Data

Improving Credit Risk Management with Nikkei FTRI's MCEX

The main business of banks is lending, making credit risk management (CRM) the most important aspect of their management. Simply put, "credit risk" refers to the risk that money lent will not be returned. Assets calculated while considering credit risk are called "credit risk-weighted assets," and banks are required to maintain a certain ratio of capital on hand relative to such assets. This kind of regulation comes from what are known as the Basel Accords, which are positioned as the fundamental regulations that support financial stability.

The first Basel Accords, namely Basel I, were implemented in the 1980s, but it was BaselⅡthat brought the refinement of credit risk-weighted assets calculation closer to the current style.*1 BaselⅡnewly adopted the internal ratings-based approach (IRB) in addition to the standard approach, which allowed banks to use internal models to calculate credit risk-weighted assets. Use of the IRB requires approval from the authorities, but many regional banks in Japan are still aiming to adopt the IRB because it offers various advantages, such as more sophisticated CRM, more efficient management, and the PR effect. However, it is known that without help, adoption and maintenance of the IRB imposes a considerable burden on employees, as statistical tests based on vast numbers of perspectives must be conducted and know-how regarding theory used in the test and results must be passed on.*2

*1 As of 2023, it is still being used in a revised framework, Basel Ⅲ.

*2 Basel Ⅲ requires validations of key risk parameters and the underlying rating system.

The best way forward is to use "MCEX" (or "Model Checker EX"). At Nikkei Financial Technology Research Institute (Nikkei FTRI), we provide MCEX, which is a statistical analysis tool that specializes in enhancement of the level of CRM in terms of both efficiency and quality. It has been supporting many banks since the early 2000s, when the transition to IRB began. We are able to offer many advantages through MCEX with confidence, including the fact that you can use our know-how for model testing and construction with no code, acquire a text book about the statistical theory behind each feature, and attend our seminars and get support tailored to your needs(see also Fig. 1).

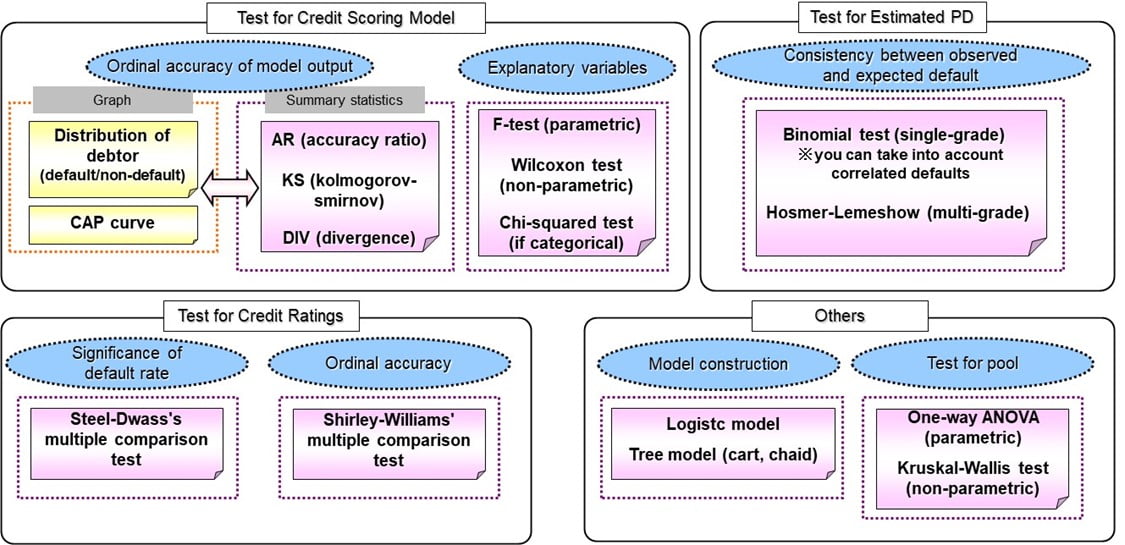

Fig 1. Comparison between MCEX and other tools

MCEX has a variety of features that are indispensable for testing and construction of the CRM system, including testing based on ordinal accuracy, which is known as the most important point, testing for ratings using multiple comparison theory, which is one of the most advanced concepts in statistics, and tree model features(see also Fig 2). These features are sufficiently qualified for advanced CRM. You can use all of these features simply by pressing buttons to select analysis settings. In addition, the "Excel Add-in function," which allows users to employ major MCEX features as the Excel function, is also available on a PC on which MCEX is installed.

Fig2. Main features of MCEX

MCEX has been widely used as an essential tool for CRM by Japanese banks for about 20 years, ever since its launch, and we have received many positive comments from users.

- ・Introduction of MCEX has reduced the time required for a CRM test from approximately 2 months to 9 hours!

- ・The time reduced has been spent understanding more detailed characteristics of scoring models. As a result, it has been found that even within the same category (production industry), performance was excellent in the automotive-related industry, but poor in the food manufacturing industry. In response to this, we succeeded in enhancing its CRM by distinguishing categories that rely on the scoring model and those that place importance on other assessments.

Despite the above comments, the environment surrounding banks' CRM has become even more complex in recent years; for example, there exist the issues of sophisticated financial fraud and how they to use AI models. We hope to contribute to the further development of banks, and thus the economy as a whole, through statistical analysis based on the further evolution of MCEX.

If you are interested in our services, please contact us.

https://www.ftri.co.jp/eng/index.html#company

Nikkei FTRI

Nikkei FTRI is a member of the Nikkei Group that works with data analysis technology. We are recognized for the high quality of our analytical and modeling techniques, which utilize both traditional and alternative varieties of data.

See More