- Alternative Data

Changes in the DEFENSE Credit Rating Index (DCRI) following the COVID-19 Outbreak

In the "Stories" section dated April 12, 2023, we reported on changes in the credit quality of Japanese listed companies from the beginning of the COVID-19 outbreak until March 2023. We used credit ratings estimated by RADAR, a quantitative rating model based on financial information from Nikkei FTRI (Nikkei Financial Technology Research Institute, Inc.). Here, we report on the same matter using the DEFENSE Credit Rating Index (DCRI) calculated by DEFENSE, another Nikkei FTRI product.

DEFENSE combines and fine-tunes data for a theoretical model (option pricing theory, Black-Scholes-Merton model) based on financial and stock price information on listed companies. It employs its own logic that considers the customs and scale of each market. The information is delivered on a daily basis with a high level of default risk capture. In addition to the aforementioned DCRI, information made available includes a score that predicts a given company's likelihood of having committed accounting fraud.

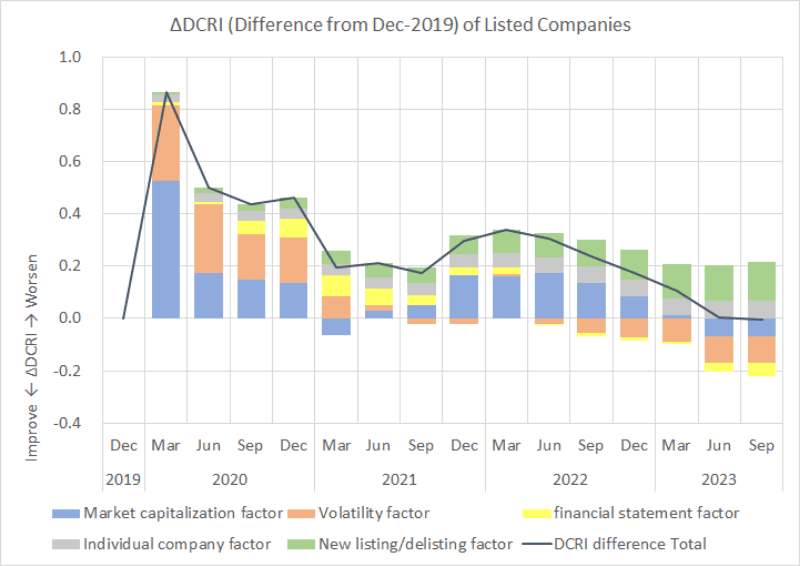

Fig. 1

The solid line in Fig. 1 displays the difference between the average DCRI value for all Japanese listed companies from the end of December 2019 to the end of September 2023, minus the DCRI value at the end of December 2019, immediately after the occurrence of COVID-19 (ΔDCRI = DCRI - DCRI at end of December 2019). Note that ΔDCRI will increase or decrease in value if it worsens or improves, respectively, in comparison with the DCRI value at the end of December 2019. The ΔDCRI had deteriorated to a maximum value of +0.87 by the end of March 2020, the quarter immediately following the COVID-19 outbreak. However, it has improved to +0.50 by the end of June 2020, following quarter. By the end of March 2021 it had further improved to +0.20, but it had deteriorated slightly to +0.34 by the end of March 2022. Thereafter, the DCRI continued to improve until recently, returning to -0.01 at the end of September 2023, which was almost equivalent to the level immediately after the COVID-19 outbreak. This trend in the DCRI is generally consistent with that for the TOPIX index, but the TOPIX index was 35.0% higher at the end of September 2023 than at the end of December 2019 - a larger figure than that indicating the impact of the improvement in the DCRI, which reflects credit quality.

The stacked bar chart in Fig. 1 shows the decomposition of ΔDCRI into five factors: market capitalization factor, volatility factor, financial statement factor, individual company factor, and new listing and delisting factor. The market capitalization and volatility factors provides stock price information, while the financial statement factor gives financial information. However, the DCRI of individual companies that changed by more than +/- 1.0 in a week were separated from the previous three factors to be considered as individual company factors. In addition, since the ΔDCRI apparently worsens or improves when a relatively low-/high-rated company is newly listed or when a high-/low-rated company is delisted, this effect is included as new listing and delisting factor. Reflecting the sharp decline in stock prices, the market capitalization factor and the volatility factor were the main factors that caused the DCRI to worsen in the quarter immediately following COVID-19, which lasted to the end of March 2020. From the following quarter, the market capitalization factor began to improve, but the improvement in the volatility factor was delayed; in 2021, the financial statement factor deteriorated as the decline in performance during the Corona disaster gradually began to be reflected in financial statements. However, the DCRI improved as the volatility factor improved; from the end of December 2021, the DCRI reached the peak of its deterioration at the end of March 2022 as the market capitalization factor worsened, but it has since begun to improve. In the most recent period, the deterioration of the new listing and delisting factor is more pronounced. Excluding this factor, the latest ΔDCRI is -0.15, which is interpreted as an improvement from the level immediately after the COVID-19 outbreak.

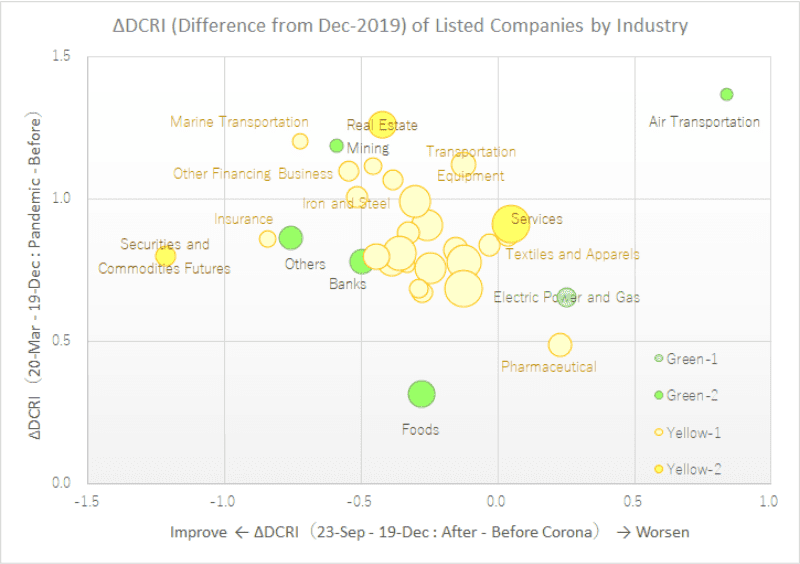

Fig. 2

Fig. 2 plots the average ΔDCRI by industry, excluding individual company factors and new listing/delisting factors. The vertical axis is labelled with the ΔDCRI at the end of March 2020, the quarter immediately following the COVID-19 outbreak, and the horizontal axis is labelled with the ΔDCRI at the end of September 2023, the most recent quarter. The size of each circle represents the number of relevant companies, and the color shows the status of the average DCRI by industry at the end of March 2020 (Green-1: aaa to a, Green-2: a- to bbb, Yellow-1: bbb- and bbb+, Yellow-2: bbb). The names of industries that deviate from the overall average for listed firms are included. The industries with the largest deterioration in ΔDCRI in the quarter immediately following COVID-19 were air transportation, real estate, and marine transportation. Air transportation continued to have the largest ΔDCRI in the most recent quarter. In contrast, marine transportation improved significantly to -0.72 due to higher freight rates and the weaker yen. The industry sector with the lowest degree of increase in ΔDCRI in the quarter immediately following COVID-19 was foods (meaning the food manufacturing industry, not the food services industry). In addition to air transportation, electric power and gas and pharmaceuticals also continued to see unfavorable conditions in ΔDCRI in the most recent quarter. The performance of electric power and gas is thought to be due to the weak yen and soaring crude oil prices. The outcome for pharmaceuticals may seem to be strange, given the recent strong performance of the TOPIX index. This reflects the fact that the DCRI by industry is a simple average of the number of companies, without considering market capitalization weightings as in the TOPIX index. As a matter of fact, there has been little improvement for mid- and lower-tier companies, of which there are many.

As described above, the DCRI, which reflects credit quality, deteriorated significantly in the quarter immediately following the COVID-19 outbreak, but we have confirmed that it has recently improved to its pre-COVID-19 level. It should be noted, however, that the degree of decline and the progress with improvement vary by industry sector.

If you are interested in our services, please contact us.

https://www.ftri.co.jp/eng/index.html#company

Nikkei FTRI

Nikkei FTRI is a member of the Nikkei Group that works with data analysis technology. We are recognized for the high quality of our analytical and modeling techniques, which utilize both traditional and alternative varieties of data.

See More