- Business Solution

- Market Data Approach

AERIS: Technology for Better Financial Statement Forecasting

AERIS is an effective and powerful tool for predicting the content of future financial statements. It was first developed by the Nikkei Financial Technology Research Institute (or "Nikkei FTRI") in June 2009.

The environment surrounding financial institutions has changed dramatically since the Global Financial Crisis (or "GFC") occurred near the end of the first decade of this century. At that time, many such organizations faced capital shortfalls due to the limited ability of traditional stress testing methods to assess capital adequacy. In the wake of the GFC, the Basel Committee on Banking Supervision (or "BCBS") made its stress testing principles publicly available, in a move that increased the value placed on stress testing. Since the GFC, international regulators have announced the introduction of various measures that include the use of risk appetite frameworks and forward looking allowances, thus drawing greater attention to stress testing in general.

Macro stress testing, which has been widely implemented by financial institutions, incorporates predictions about future changes in the macroeconomic environment. In a typical macro stress test, future rating transition matrices are projected based on those of the past, and capital adequacy is evaluated with an eye to credit portfolio changes. However, this method can only capture alterations of a credit portfolio as a whole, and it does not allow drilldowns to the level of the credit fluctuations of individual companies. Scrutiny of change to credit portfolios considered as collective wholes remains important. However, since macro stress testing incorporates predicted future shifts in the macroeconomic environment, there is also a need to use its results for formulating specific support measures for individual companies in response to changes in their unique credit conditions.

Despite the fact that credit changes to both portfolios and individual companies are vital checkpoints for financial institutions, many have not been able to develop time-efficient systems for bulk financial statement forecasting. AERIS is a product that a number of financial institutions use to solve this problem. AERIS forecasts the financial statements of the large, medium, and small corporate entities that make up individual credit portfolios. It allows the user to instantly gain a picture of credit-portfolio-level change while also learning which companies have risen or fallen in credit rank.

AERIS forecasts financial statements using only three parameters drawn from future macro stress scenarios. In addition, such resulting predictions themselves can also be used to estimate credit ratings, and the system automatically calculates credit costs and Common Equity Tier 1 ratios. AERIS gives users the capability to conduct macro stress tests faster and more efficiently than ever before. In recent years, AERIS has been used not only for the aforementioned tasks, but also for forward looking allowance and climate change risk measurement.

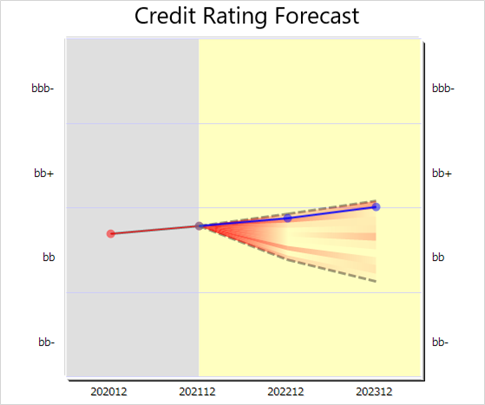

The graph below shows credit rating change based on forecasted financial statements. The dotted lines indicate the upper and lower limits of the credit ratings predicted by the simulation, and the blue line signifies the most likely credit ratings. Based on the range of the predicted movement of credit ratings, this type of graph can be employed to support the business of companies that are concerned about credit deterioration due to the COVID-19 disaster.

We invite you to try AERIS on your own credit portfolio. If you are interested, please contact us.

https://www.ftri.co.jp/eng/index.html#company

Disclaimer (PDF file):

https://www.ftri.co.jp/eng/pdf/SMACOM_Disclaimer-EN.pdf

Nikkei FTRI

Nikkei FTRI is a member of the Nikkei Group that works with data analysis technology. We are recognized for the high quality of our analytical and modeling techniques, which utilize both traditional and alternative varieties of data.

See More