- Alternative Data

- Market Data Approach

SMACOM's new momentum score under development

As noted in an earlier article, factor investing has been the subject of much research and experimentation, especially in equity markets, and it has been widely deployed in the asset management world. While our previous focus in this area was value factor, here we will discuss momentum factor, which is another major topic in the world of factor investing.

In the field of finance, momentum can be broadly divided into the two categories of stock price momentum and earnings momentum. The former term is used for the phenomenon whereby, when looking at past returns, past winners tend to outperform past losers in the intermediate term. The latter expression refers to the indicative nature of large earnings revisions when considering subsequent earning revisions and price drifts.

Regarding stock price momentum, academic research in the U.S. has shown that strategies of buying winners (i.e., stocks with the highest returns) and selling losers from the most recent 3- to 12-month period tend to generate significant positive returns over the subsequent 3- to 12-month period. This phenomenon is called medium-term price momentum. However, further studies have demonstrated that past winners tend to underperform past losers in the first month following portfolio construction. This phenomenon is referred to as short-term price reversal. In Japan, however, the reversal effect has been observed both in the medium and short terms. When examining earnings momentum, in Japan as well as in the U.S., it has been found that stocks with large upward earnings revisions tend to subsequently experience positive abnormal returns. Other academic literature has documented cases in which earnings announcements exceeded (or fell short of) analysts' forecasts by large extents and stock prices increased (or decreased) not only at the time of announcement, but also over the medium-to-long term period thereafter.

Behavioral finance is often referenced to explain such momentum effects. Medium-term momentum is said to be caused by earnings momentum and by investors' initial underreaction to information being corrected in the medium term, while short-term reversal is explained as a result of by short-term investor overreaction.

As with previously noted issues related to value factor, this paper considers market beta, size, and book-to-market ratio plus size-related nonlinear factors to be systematic risk factors, following Fama and French (1993). It examines whether momentum factor information excluding such risk factors has cross-sectional predictive power in relation to stock returns.

Three momentum factors - price reversal-based, price momentum-based, and earnings momentum-based - are used as alphas. These are risk-adjusted alphas constructed with our own methodology to exclude the four systematic risk factors noted above. The investment ratio (or weight) of each stock has been calculated with the assumption that the target portfolio risk is 5% annually. The investment universe is composed of the stocks listed on the Tokyo Prime market (i.e., what was formerly known as the first section of the TSE), excluding those in the financial sector, and the backtesting sample period is from January 2007 to September 2022. The rebalancing frequency is monthly, and transaction costs are not considered.

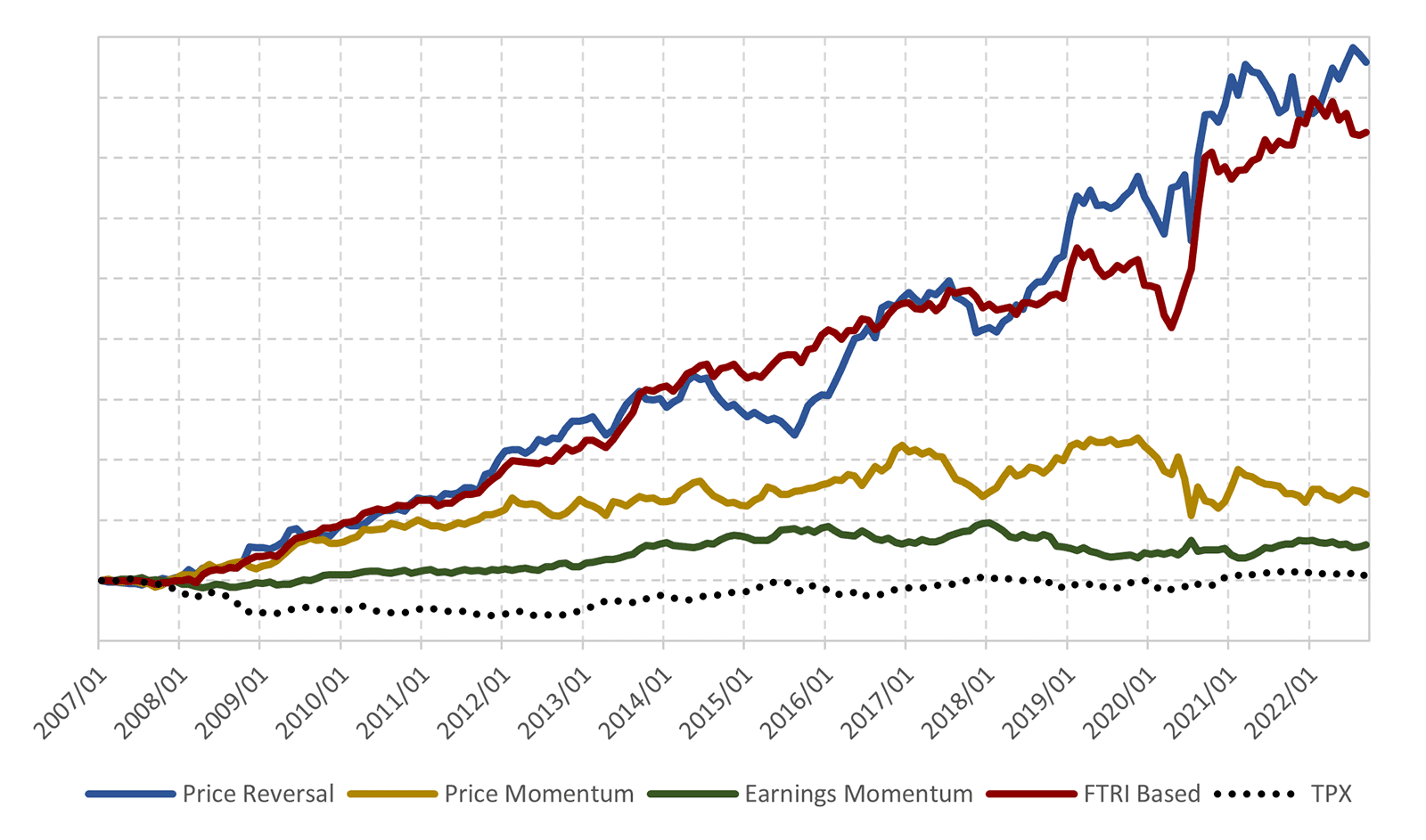

Figure1 Performance of momentum (reversal) factors

Figure 1 shows the performance of each momentum factor, plus an FTRI-based factor that is a composite of the three such momentum factors. The composite weight is calculated according to original FTRI methodology. "TPX" indicates TOPIX as a reference. The results demonstrate that all of the factors outperformed TOPIX. The risk-return ratio (or information ratio) for each of the three value factors is also higher than that of TOPIX's, especially in the case of the price reversal-based factor, at around 1.05 (excluding dividends). This indicates that the reversal effect is in line with that predicted by past literature, even after excluding the four systematic risk factors noted above from the price reversal factor.

Next, note that the risk-return ratio for the FTRI-based factor is 1.30, which demonstrates an improvement in risk-adjusted return. This suggests that the correlation among the momentum factors, especially between price reversal and earnings momentum, is low (i.e., negative), which may be the causal element accounting for a more efficient portfolio with lower risk.

The value factor was the focus of the previous article, and the momentum factor has been discussed here. Another major issue in question is the quality factor, which will be explained later. The final matter of discussion is the supposition that a composite thereof (i.e., the value, quality, and momentum factors) based on the IC (Information Coefficient) can lead to a more efficient portfolio from a risk-return perspective.

SMACOM: https://www.ftri.co.jp/product/smacom/en

SMACOM free trial (below):

https://www.ftri.co.jp/eng/index.html#company

Disclaimer (PDF file):

https://www.ftri.co.jp/eng/pdf/SMACOM_Disclaimer-EN.pdf

Nikkei FTRI

Nikkei FTRI is a member of the Nikkei Group that works with data analysis technology. We are recognized for the high quality of our analytical and modeling techniques, which utilize both traditional and alternative varieties of data.

See More